Naomi Ballantyne

Partners is no longer paying override commissions to dealer groups. This is likely to have a major impact on some groups which relied on these commissions to run their businesses.

These payments, and fixed dollar marketing support, will stop on July 1.

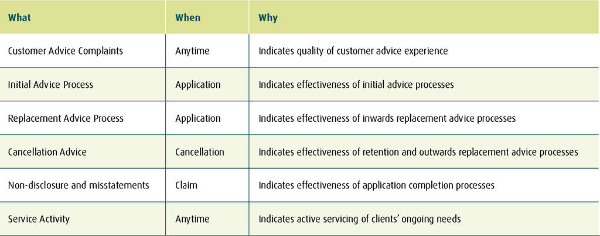

Instead the life company will pay overrides to FAPs and payment will be made based on customer outcomes including initial advice and replacement advice process, cancellation advice, non-disclosure and misstatements, service activity and customer advice complaints.

“We are redirecting all previous over-riders and fixed dollar support payments into FAP over-riders (FAPOs) which will be payable to FAPs.”

These overrides will be based on the bonus commissions earned by the advisers within the FAP.

“This financially aligns the interests of advisers and their FAPs with customer outcomes.”

Partners Life managing director Ballantyne says these changes and some changes to commission structures are about who gets the money, rather the quantum the company pays out.

“It is the same amount of money in the system,” she says. “the difference is whose hand it goes too.”

In the past money had gone to dealer groups but hadn’t been used in the way it was intended. Under this model the adviser will make the decision how to spend the money to grow their business.

There is potential criticism that the money won’t be spent on the business, but Ballantyne doesn’t think this will be a big issue as adviser are facing increased costs and will need support.

Ballantyne says the changes are being made in response to pressure from the regulator.

“The regulator thinks that upfront commissions are too high and can incentivise poor adviser conduct.

“We want to demonstrate that commission can incentivise good adviser conduct.”

She says advisers will face increased costs in running FAPs, and these changes are designed to support FAPs.

Partners Life has been encouraging advisers to be become FAPs through the transistional licencing process.

“We are encouraging as many advisers as possible to become their own FAPs,” she says.

If they have a licence then they are keeping their options open.

Measuring customer outcomes

Partners has developed a points matrix to help measure customer outcomes and this will be released soon.

Measurement and reporting on these outcomes will start on April 1. However, scaling of the commission bonus will not start until March 31 next year.

This one year transition period is designed to facilitate an understanding of customer outcomes being achieved by each adviser and to provide a reasonable time period for advisers to adjust their business practices.

Advisers will get feedback each month on how they are going.

Ballantyne says the process will “encourage people at the bottom to change their behaviour.”

Adviser bonus commission rates will remain at current levels during this period.

Partners will be contacting clients at application time to measure an adviser’s performance. Ballantyne said was wasn’t appropriate for the company to be involved in the process earlier as that would be a potential conflict.

“We are not expecting to find a lot of issues,” she says. However, when they do they can help the adviser improve their processes.

She expects that there will be pushback from some advisers, but they have nothing to fear if their advice process is good.

| « Partners puts hold on redundancy cover | Mixed reviews from advisers on FMA regulation » |

Special Offers

Sign In to add your comment

© Copyright 1997-2026 Tarawera Publishing Ltd. All Rights Reserved

Well said Naomi. Unlike the banks it’s great to see an insurance company get their head around what licensing is supposed to be all about. Licensing of the financial services industry was never designed with dealer groups in mind. A dealer group does NOT give advice to your customer, YOU the adviser do. Licensing is supposed to be about holding to account the individual giving the advice. That can never be applied to a dealer group without significant consequences to the adviser and his or her business.

Most dealer groups are mortgage aggregators whose focus is supposed to be on their mortgage advisers. However, override payments from the insurers have become very lucrative with up to 30% of the API been paid on a policy issued by an adviser. When you consider the combined API production of various groups members it’s big money for these dealer groups to have going into their coffers every month. Whilst some of the groups like Newpark have been investing this money back into their members businesses most of the dealer groups have not.

Partners Life has just signalled to the industry that payment of the override will now go to the adviser directly if they elect to become their own FAP as opposed to them working under a dealer group FAP. Insurance and mortgage advisers who have perhaps been quietly sitting on the fence about whether to work under a dealer group FAP or become their own FAP have probably just had their minds made up for them with this news. When advisers start crunching the numbers in terms of extra revenue earned it’s a no brainer. We can clearly see now why dealer groups such as Astute, Kepa, Mortgage Link and NZFSG have all been encouraging their members to work under their dealer group FAP licences. The monetary incentive from overrides means these dealer groups simply do not want their members opting to become their own FAP.

When insurance companies like Partners Life will now deal directly with you under you own FAP and pay you the override commission which was formerly only available to dealer groups why would you still elect to work under a dealer group FAP? The amount of support been provided to advisers nowadays by Partners Life around regulation, compliance and the advice process dwarfs anything that the dealer groups are offering to their own members. Let’s not forgot Partners Life has also made available at no cost to accredited advisers the wonderful adviser support programme to help advisers through licensing. With all the money that dealer groups have been making from overrides over the years it’s telling that none managed to provide an adviser support programme to their members to match what Partners Life created at their own expense.

With a FAP been legally responsible for the advice that it will give to customers any adviser who elects to work under a dealer group FAP will essentially become a quasi-employee. Just think about that for a second and what it means for you and your business. Most advisers in New Zealand operate their own businesses and want to continue trading under their own established names. Working under a dealer group FAP licence will be the first step to you losing this independence. To think otherwise is naïve. In time you will be changing the name above your door to whatever your dealer group master wants you to. And meanwhile that override commission that you could have been earning yourself now is still going into your dealer group’s own pockets.