Equal weight vs. Market cap weight

Investing: What’s your optimum weight?

Tuesday, November 27th 2018, 9:07AM

by Pathfinder Asset Management

Karl Geal-Otter

Indexing has become mainstream and an increasingly popular way to invest in capital markets. It’s cheap, tax efficient and gives you roughly the same return as the market. Most portfolios track an index that is weighted based on market capitalisation (cap-weighted); individual weights are determined by dividing the company’s market cap by the sum of all constituents’ market caps. There is a growing trend in the academic and investing community that this weighting method could be suboptimal. Could an alternative approach add value to a passive portfolio?

Equal weighting is simple – a portfolio holds the same dollar value in each stock meaning each stock represents an equal value in the portfolio. Each individual stock has the same influence on performance and the results are positive, demonstrated by the graph below. The graph looks at the popular MSCI ACWI Index (orange) compared with the MSCI ACWI Equal Weight Index (blue) over a 20-year time horizon (since inception for the equally weighted index); the equally weighted index outperforms by 2.8% per annum over this period.

This method of weighting a portfolio has long been studied by academics and practitioners. There is a range of explanations as to why equal weighting adds value over a traditional cap-weighted portfolio. Four key factors are:

- Inefficient markets

- Avoiding concentration in a few “big names”

- More exposure to small cap

- Mean reversion through rebalancing

The first point is a contentious one amongst academics and the wider investment community. The inefficient market theory argues against cap-weighting because it over-allocates to stocks whose price is high relative to its fundamentals, and underweights low-priced stocks relative to its fundamentals. The efficient market debate will likely go on forever and is not the aim of this article. The last three factors, however, do provide for sensible discussion and will be the focus of this article.

Avoiding concentration

Cap-weighted portfolios have a higher concentration to the largest companies. This dynamic assumes that yesterday’s winners will continue to win. If we look back over the makeup of the S&P 500, we can see how this isn’t true. In the ’80s, the top 10 holdings were dominated by energy companies like Exxon, Shell and Mobil - nowadays, technology companies dominate with 5 representatives. Those top 10 companies now represent 22% of the total S&P 500, equal weighting can help reduce this concentration risk. By spreading an equal value across all companies in a portfolio you are placing an equal bet on each company’s success – a passive decision.

The downside, however, comes from periods we have just experienced, where the largest companies (and weightings) are all in the same sector (technology) which has outperformed by a large margin, resulting in short-term outperformance by cap-weighted portfolios compared to equal weighted portfolios.

The conclusion, the first benefit of equal weighting is a risk mitigant – don’t put all your eggs in one basket – or in this scenario don’t put more eggs in a select few baskets.

Small-cap exposure

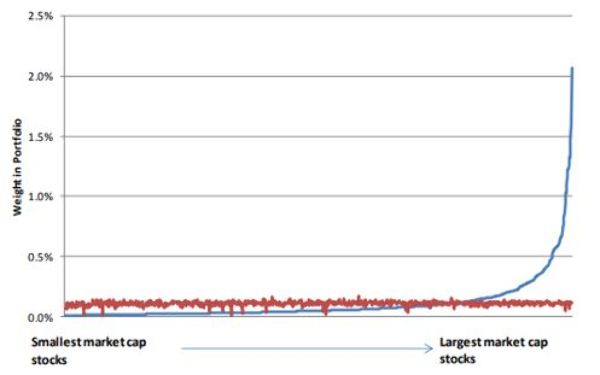

Because a cap-weighted portfolio is biased towards large companies, they naturally hold a low weighting in small-caps. Over long time periods, this has been costly. Over the past 20 years, the MSCI World Small Cap Index has outperformed the MSCI World Index by 4.4% per annum. Adjusting for risk, the Sharpe ratio of the Small Cap Index is also better, 0.3 vs 0.1 (assuming a risk-free rate of 2%). The graph below is a good representation of how the weighting differs between an equal and cap-weighted portfolio (source: MSCI research). The blue line represents a cap-weighted portfolio; as we move to the right the individual weights increase significantly. The red line is the same portfolio, but equally weighted, and has a larger weight on the left-hand side (small-cap companies) and is equal across the spectrum of market capitalisation.

Small caps, as an asset class, are more volatile, but over long-time horizons, they add risk-adjusted value to a portfolio – equal weighting seeks to capture this alpha compared to a traditional cap-weighted approach. A long-term positive and a benefit based on return.

Mean reversion

Mean reversion is the idea that over time, asset prices or other financial metrics revert to their long-run mean. A stock price that has risen significantly, by definition, has a lower expected return. Within an equally weighted portfolio, mean reversion plays a big part in alpha generation. Unlike a cap-weighted portfolio that evolves over time with stock price fluctuation, an equally weighted portfolio must be regularly rebalanced to bring companies back to equal weight following price moves.

Trimming recent winners, and adding to recent losers, adds a contrarian view, betting against Wall Street. The frequency of reweights could be minutes (high-frequency trading), days, weeks, months or even annual. In a perfect academic world, we could find the optimal reweighting frequency that considers the natural momentum of stock price moves. This would be difficult in the real world with transaction costs, tax implications and time.

Building a disciplined portfolio rebalancing framework will take advantage of mean reversion of stock prices. An example of a common rebalancing frequency is quarterly. This is deployed by the large index providers as it fits in with their cap-weight index reviews (removing or adding companies) which typically happens on a quarterly basis. It is important to read index and ETF methodologies to understand how often your investment could be rebalancing. Anything more than monthly could result in excessive trading costs that eat away returns.

To recap our three factors, avoiding concentration in large names is a risk mitigant that improves overall diversification. Allocating a larger weight to the small end of capitalisation is a return generating factor. Finally, rebalancing a portfolio at regular intervals take advantage of mean reversion a long-standing economic theory. Rebalancing frequency becomes an important decision in the portfolio construction process.

The downside of Equal Weight

Increased returns, means increased risk. The major downside for equally weighted portfolios is the increased volatility, predominantly from the small-cap bias. Although this has been shown to add value over the long-term, some asset allocators operate with volatility constraints – it is important to consider the impact of increased volatility on an entire portfolio. The second thing to consider is the rebalancing. Two negatives can arise from this: (1) transaction costs; not only would weekly rebalancing be a large constraint on time, but the transaction costs would also pick up significantly – potentially erasing alpha. (2) the behavioural aspect can be difficult without having mental models in place; rebalancing requires selling stocks that are on a roll and adding to losing positions. For some people, this might be easy once or twice, building a robust model to remove emotion from the continuous rebalancing is vital. Liquidity should also be considered when running equal weighting. An increased weight to small caps could restrict the growth of the fund.

Investment Options

The modern world of investing means there is often an ETF available for an alternative way to gain exposure to the market. Equally weighted ETFs are no different. The performance numbers used at the beginning of this article tracked the MSCI ACWI Equal Weight index, this is available through the ETF Guggenheim ACWI Equal Weight (ticker: EWAC). Other ETF options include Invesco Equal Weight S&P 500 (ticker: RSP), VanEck Vectors Equal Weight Australia (ticker: MVW) and iShares MSCI USA Equal Weight (ticker: EUSA), to name a few. In actively managed mutual funds, portfolio managers can equally weight their investment ideas, although this isn’t very common in the New Zealand market.

Karl Geal-Otter is an investment analyst at Pathfinder Asset Management, a boutique responsible investment fund manager. This commentary is not personalised investment advice - seek investment advice from an Authorised Financial Adviser before making investment decisions. Disclosure of interest Pathfinder Asset Management’s Global Responsibility Fund uses equal weighting methodology.

Pathfinder is an independent boutique fund manager based in Auckland. We value transparency, social responsibility and aligning interests with our investors. We are also advocates of reducing the complexity of investment products for NZ investors. www.pfam.co.nz

| « Time to invest in gold? | The Third Scenario – The End of Goldilocks » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |