- emerging sharemarkets down 15% in a 10 day period in mid-May;

- the Japanese sharemarket down 11% so far from its six year high in April;

- European shares at a four month low in late May;

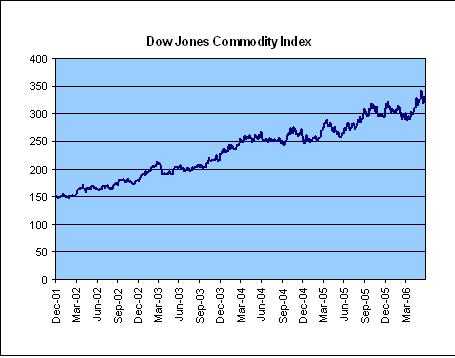

- commodities having their largest weekly fall in 25 years in mid-May (CRB Index).

A key reason for this is the reversal of speculative excesses in some markets. However, there is also a growing concern that the “goldilocks” US and global economic outlook (good growth without associated inflationary issues) may not occur going forward. Instead there are concerns that a scenario of too much growth and inflation will lead to continuing co-ordinated Central Bank interest rate rises. Also, there are some in the market who are fearful of stagflation (high inflation and interest rates and low growth).

After the incredible returns from various global markets over the past few years (and the significant speculation entering some markets) a sell-off is not a huge surprise; although very difficult to time exactly! But is this the start of a bear market phase or just a necessary correction to release some of the steam from over cooked markets?

The case for this being “just” a correction only is as follows:

- Co-ordinated global growth. This is shaping up as the most balanced growth period for some time with global GDP set to be around 4% for the next two years, with all regions contributing. The strong global growth profile contrasts markedly with New Zealand’s outlook.

2002a

2005a

2006f

2007f

United States

1.6

3.5

3.5

2.6

Euroland

0.9

1.4

2.0

1.7

Japan

-0.3

2.7

3.2

2.9

Australia

4.0

2.7

3.7

3.5

China

8.2

9.9

9.6

9.1

World

2.8

4.2

4.3

3.8

New Zealand

4.8

2.2

1.2

2.4

Source: Statistics NZ, RBNZ, GSJBW

- Strong company earnings. Corporates are in strong shape both in terms of earnings growth and their balance sheets. The latest US earnings round generally saw a record number of positive surprises and the outlook remains for double digit earnings growth into 2007.

- Markets are not over priced. While there are obvious speculative excesses in the commodity and emerging markets the major global sharemarkets are not expensive. In fact the US market P/E has contracted consistently over the past four years.

Price/Cash Earnings

Region

Current

20 Yr Range

US

12.2

6.3-19.7

Japan

10.8

7.1-18.4

MSCI Europe

8.4

6.6-16.0

Source: Capital International

- Productivity. A key measure of productivity is unit labour costs (ULC) and these have been trending the right way. For an extreme example one can look to Japan where ULC’s are at their lowest in almost 20 years! ULC’s are also declining in economies as diverse as Germany and Singapore and are slowing in the US.

The case for this being the start of a bear market is:

- Global imbalances. The large twin deficit problem for the US is nothing new but it seems Europe is joining the party with its trade deficit with China now almost as large as the US.

- High consumer debt. Again this issue has been around for a while but throw in rising interest rates and an end to double digit rises in residential house prices and the importance of this issue increases.

- Housing slump? After running hot for a sustained period, the US residential housing market is slowing but will it turn into a slump? A strong case can be made that this could happen although a repeat of Australia’s experience (a slight sell-off) is more likely.

- A commodities bubble bursting? This was one of the more interesting aspects of the May sell-off with copper coming off all-time highs, as did aluminium (off a 17 year high) and nickel and zinc off record levels as well. Speculation (hedge fund driven?) in the derivative markets has created a roller coaster ride. However, the underlying commodity price picture still looks positive because of the huge latent demand from Asia, and China in particular. While there will be a supply side response being a commodity producer is still likely to be a good place to be over the coming decade.

- One-off shock potential. This is always an inherent risk in investment markets, with Asian flu, Iran’s nuclear aspirations and terrorist threats ever present.

- Chinese growth peaking. The China growth story is a wonderful one for the global economy but it may not be all plain sailing. As much for political (growing rural unrest at income inequalities) as economic reasons the Chinese Government and Central Bank are looking to slow things down. It is a huge economy to centrally manage and the best case is probably for it to slow down from almost double digit economic growth to still robust growth (in the 6-9% pa range). However, there are real excesses in that economy and so managing this slow down could still go awry. Moreover, the need to manage the revaluation of the Chinese currency adds to the complexity.

So how does New Zealand look under these varying global scenarios?

While the New Zealand sharemarket has done very well over the past three years (23% compound growth for the NZX50 Index), it does not seem to have been caused by any speculative bubble. We have been relatively immune from any extreme excesses of the commodity and emerging market boom, just as we were from the dot com bubble bursting. Having said this we were vulnerable to a sell-down given the significant upwards P/E re-rating we have enjoyed relative to the rest of the world (as highlighted in last month’s commentary).

While we are going through a recession at present, it is a shallow one and we do not look like we are heading for a hard landing. Instead the positives of continuing strong global economic growth and a weaker Kiwi dollar means that the export sector should be robust. This is the traditional way for the New Zealand economy to come out of a recession (a pick up in the country before moving into the city) and it looks like being repeated in 2007. Any further lift from a recent pick up in immigration will further help matters.

So my conclusion is that while we can expect more volatility over the coming months than the relatively low levels of recent years, the long-term outlook for global sharemarkets looks sound. One could try to time this by trading in and out of market fluctuations but for most investors I believe the best strategy is to keep to a long-term perspective as the rewards should be there – albeit not as stellar as they have been in recent years.

Source: Bloomberg To see how the numbers stacked up for various markets around the world in the past month and over the year, visit our