Releasing the Handbrake

Friday, October 9th 2015, 3:30PM

by Harbour Asset Management

A key theme in the NZ fixed interest markets over the past 12 months has been the absence of inflationary pressure, turning the chance of further OCR hikes into the series of OCR cuts.

Ahead of the September Monetary Policy Statement, the RBNZ’s approach had been to apply a handbrake on the market getting too far ahead of itself. In his last speech, the Governor had highlighted that to forecast aggressive OCR cuts the RBNZ would need to be forecasting a recession. At that stage, the RBNZ wasn’t really even forecasting a slowdown at all – more a case of the economy continuing to grow at 3%, supported by historically low interest rates.

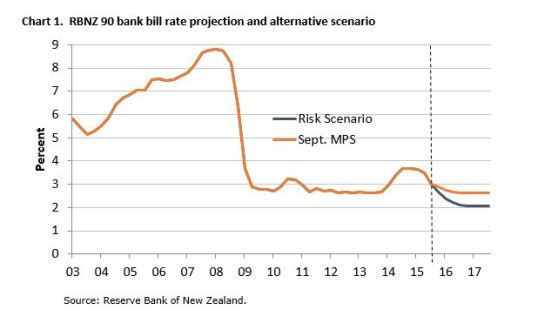

At the September Monetary Policy Statement, the RBNZ eased some of that pressure by releasing the handbrake a little. As expected, the RBNZ cut the OCR to 25 basis points to 2.75%. However, it was the more dovish forward looking messages that took the market by surprise:

• The RBNZ signalled that “some further easing in the OCR seems likely”.

• Its forecast of the 90 day bank bill rate implied another OCR cut to 2.50%.

• It provided an alternative scenario which included more aggressive cuts in the OCR to 2.00% (see Chart 1).

The market interpreted the Statement as making another 25 basis point cut at the December MPS highly likely, with a chance this gets brought forward to the October OCR Review if the economic data continues to deteriorate. More generally, it changed the perception that the RBNZ was uncomfortable with the OCR getting below 2.50%.

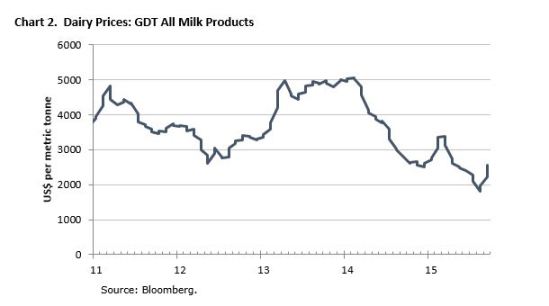

A key driver of the change in tone from the RBNZ was its view on dairy prices, and the implications for its projection for growth and inflation. Following sharp falls in dairy prices from June to early August, the RBNZ took a conservative approach and assumed within its central projections that diary prices would remain at those levels for a considerable period before rising to more sustainable levels.

However, since their projections were prepared, dairy prices have bounced back around 40% (Chart 2). Fonterra has also revised up its 2015/16 dairy payout forecast by 75 cents to $4.60. While dairy prices are still at levels that are restrictive for dairy sector profitability and cashflow, they are less restrictive than those baked into the RBNZ’s forecasts, making an October OCR cut less likely than otherwise; and certainly not a “done deal”.

The next key piece of data for the RBNZ is Q3 NZ CPI inflation on 16 October, with the market expecting 0.3% for the quarter and 0.2% annual inflation.

In coming quarters, the NZ CPI inflation is expected to rise back into the RBNZ’s target range above 1%, in part as the sharp falls in oil prices in Q4 2014 and Q1 2015 roll out of the annual inflation measure. The 15% fall in the value of the NZ dollar from its peak should also help lift the prices of imported consumer goods and services.

Looking further ahead, the bigger question is whether there is sufficient inflation pressures to keep inflation near the 2% mid-point of the RBNZ’s target range.

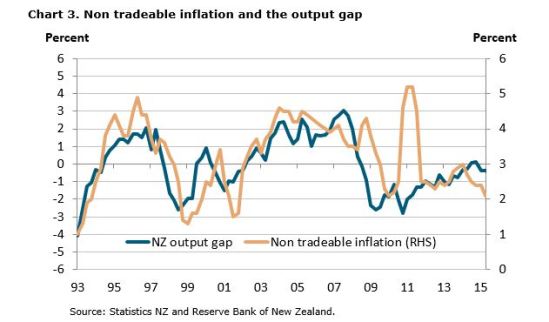

Measures of underlying inflation, like non-tradeable inflation and inflation expectations surveys are still low by historic standards; especially considering the lack of spare capacity in the NZ economy (Chart 3). A continued absence of domestic inflation pressures would keep the OCR lower for longer.

GLOBAL UNCERTAINTY UNRESOLVED

The main global event for fixed interest markets in September was the US Federal Reserve FOMC meeting, which was billed as the most important US interest rate decision since rates were cut to an all-time low of 0.25% over 6 years ago.

Global markets were on tenterhooks for weeks. For the first time since the GFC began, there was a real chance that US policy makers would start removing stimulus from the market.

A little over a month ago, around 80% of US economists expected that the US Fed would start lifting interest rates in September. However, the US Fed’s decision started to look much less certain following the sharp falls in global equity markets in August.

What started as a correction in an overheated Chinese equity market, turned into a widespread fall in commodity prices, concerns about global growth, and worries about other emerging markets.

Uncharacteristically, both the IMF and the World Bank waded into the debate, cautioning the US Fed that now was not the right time to lift US interest rates.

On the other side of the argument, the Bank for International Settlements (the central bank for central banks) publicly encouraged the US Fed to just get on with the job: in their view, markets had become too dependent on policy stimulus for too long; cheap money and easy debt were the causes of the GFC, not the solutions.

In the end, Janet Yellen and her colleagues at the US Fed took a cautious, dovish approach, and emphasised that they will be watching the global economy and markets carefully. However, they have very much left the door open.

Their published forecasts show that the vast majority of the policy committee still expect the first interest rate rise to occur in 2015. Indeed, in a speech following the decision, Yellen confirmed that it is her personal preference to lift the Fed Fund rate this year; New York Fed President, Bill Dudley, also re-iterated that the October FOMC meeting is very much a live decision.

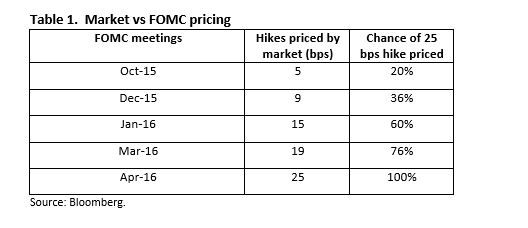

However, at the moment, the market is only placing a small probability on a rise in the US Fed Funds rate: 20% chance of a 25 basis point hike by October; 36% chance by December; and only 100% priced by April 2016 (Table1).

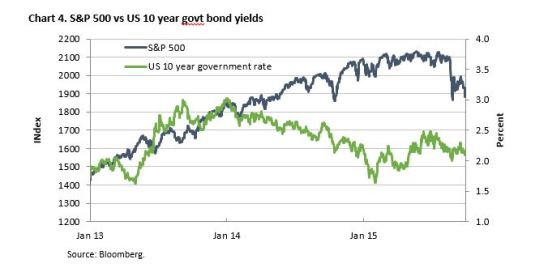

As such, the implication is that if the US Fed delivers on the plan it set out in September, then there is scope for US bond yields to rise, and lifting the NZ 10 year government bond yield off its current level near all-time lows.

REPRICING OF NZ CREDIT SPREADS

The combination of slower Chinese growth, falling commodity prices and weaker equity markets has flowed through into global credit markets. Mining company Glencore came under particular pressure, but wider credit spreads were a market-wide phenomenon.

The price action suggests the market senses a riskier environment. Investors are also aware that countries such as Saudi Arabica and China, for various reasons, are liquidating investments to generate cash.

In New Zealand, a new 5 year bond deal from ANZ sold at swap + 95 basis points, which represents about a 20 basis point widening from levels on similar debt 3 to 6 months ago. This aligns NZ bank debt with pricing in Australia, which is something we have been anticipating for a few months. However, the global credit stress has not manifested itself more widely in the NZ market.

Overall, NZ credit spreads have not yet widened relative to NZ government stock, as global demand for NZ government stock abated through September, and the market is wary of the upcoming supply from the syndication of a new NZ government bond maturing in 2033. If global credit stress worsens, we would expect NZ credit spreads to also widen versus NZ government stock.

This column does not constitute advice to any person.

Important disclaimer information

| « Nikko's new house view on global equities moves to neutral | Managers behaving badly » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |