Finely balanced, markets walking a tightrope

The Harbour team examine market movements in the past month, and what they are watching going forward.

Thursday, July 18th 2019, 6:00AM

by Harbour Asset Management

Key developments

Global equity markets performed strongly in June with the MSCI World index (in local currency) returning 5.9% over the month. Early in June markets were assured by the US Federal Reserve (the Fed) Chair that the Fed will “act as appropriate to sustain economic growth”. While these words are unlikely to become as influential as ECB Chair Mario Draghi’s “whatever it takes” comments in 2012, they were enough to make investors feel comfortable with softer economic data in the knowledge (or hope) that the Fed will be there to underpin growth. A likely source of volatility in the next 12 months is whether the market’s definition of appropriate action is the same as the Fed’s.

New Zealand and Australian share markets lagged the broader global developed market index but still delivered strong local currency returns of 3.9% and 3.7% respectively. Lower interest rate expectations further enhanced the attractiveness of higher yield names in the New Zealand market with Meridian up 20.8%, Auckland Airport up 12.4% and Meridian up 12% over the month. Low yields also led investors towards listed New Zealand Real Estate securities, with the index returning 6.2% over the month.

The strong rally in global share markets was despite economic data surprising to the downside, particularly in the US. During June, we saw more evidence of a slowdown in the US manufacturing sector with a weaker than expected ISM index reading; however, we acknowledge non-manufacturing remains strong. The US labour market showed its first sign of cracks with a weak ADP Payrolls read and consumer confidence disappointing to the downside, with trade tensions taking their toll.

Domestically, the RBNZ left the OCR at 1.50% at its June meeting, while sending a clear message that at least another rate cut is likely given the backdrop of slowing domestic and global data. At present, the market expects two cuts in New Zealand compared to four expected in the US.

What to watch

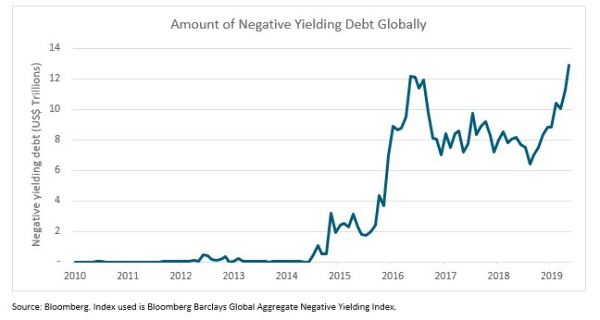

In New Zealand we’ve long had the pleasure of banks paying us to hold deposits and our government paying us if we decide to lend them money in the form of government bonds. Fewer and fewer countries around the world have this pleasure. At the end of June, 17 countries had negative yielding debt outstanding with a total market value of close to US$13 trillion. Negative debt now comprises 23.6% of outstanding investment grade debt. Low and negative yields have implications for the valuations of other assets, which are currently priced on the expectation of lower yields due to weaker economic data and inflation. If we see a reversal in data, interest rate expectations can change quickly given their low starting point. While there is no evidence of a turn in the data at this point, it pays to remember that it was only a matter of months ago when two rate hikes were expected in the US in 2019.

The G20 summit at the end of June provided some respite for those worried about the trade tensions between the US and China intensifying, when Trump relaxed his ban on US companies doing business with Huawei. At this juncture there is little doubt that trade tensions are having a measurable impact on capital expenditure, business and consumer confidence, as evidenced by recent economic data. Where there is more doubt is how the trade negotiations will play out from here. On one hand we could have a utopian win-win trade deal, an outcome that, admittedly, has a low probability at this stage, which will likely see some of the cuts currently priced-in reversed. On the other hand, we could see intensification which could lead to rates dipping further still. The answer is likely to lie somewhere in between.

Market outlook and positioning

Over the past several months, global economic data has surprised to the downside leading to lower expected interest rates across many economies. New Zealand is not exempt from the global concerns. This is despite the fact that, to date, we do not appear to be experiencing material challenges with our access to export markets. Currently, our terms of trade, production volumes and ability to sell product is in good shape. Domestically, the housing market appears to be finding a floor and the construction pipeline is solid. However, business confidence remains weak and in early July the NZIER’s Quarterly Survey of Business Opinion registered the lowest confidence reading since 2009. Gradually the economic environment domestically has shifted from one of strong growth, capacity constraints and cost pressures to one of moderate growth with some downside risk.

Within our fixed interest portfolios, we have been mindful of the sustainability of the rally in bonds and have not been willing to position for continually lower yields. Our assessment is that the New Zealand economy just isn’t in such poor shape to justify such low yields. As a result, our present strategy is to reduce duration if yields fall or if growth and inflation data pick up.

For our equity portfolios, we are increasingly wary that current asset pricing generally suggests lower future expected returns. While NZ bond yields stay below 2%, it may be rational for earnings yields to remain low. Hence extended price to earnings ratios may be here to stay. So, while relative to history it seems extraordinary that quality companies like Meridian Energy and Auckland Airport trade at 42 times this year’s earnings, in our opinion these rich valuations reflect ample global liquidity and, in many markets, negative interest rates. The Harbour portfolios generally remain concentrated in growth companies with a strategy of also maintaining exposure to several larger quality defensive investments.

In multi-asset portfolios, there is a modest underweight to equities. Within equities, while we continue to marginally favour global shares on valuation metrics, the scale of the overweight is modest acknowledging that, despite favourable valuations, these shares are likely to be more sensitive to global macroeconomic shocks.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « A narrative to take markets higher | Countdown to Brexit: Will the UK Leave on Halloween? » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |