Three themes a top fund manager is watching closely

Markets are full of conflicting message at the moment. In this feature the Harbour Asset Management team explain what's happening and how the are positioning their portfolios.

Sunday, October 13th 2019, 1:56PM

by Harbour Asset Management

Global share markets bounced back during September with the MSCI World recovering from August’s falls to return 2.3% in local currencies. A feature of global markets during the month was the resurgence of value stocks, with the MSCI World Value index outperforming the Growth index by 3.3% over the month. This reflected a combination of factors, including increased potential of a US-China trade deal and extreme relative valuations.

Global manufacturing data has continued to worsen. While Europe has showed signs of weakness for some time, the US has recently joined the fray with the ISM Manufacturing PMI contracting in both August and September, following 35 months of expansion.

Chinese manufacturing PMI came in slightly better than expected, though still in contraction territory, at 49.8 (vs. 49.6 expected). The Caixin Manufacturing PMI, which tends to capture less SOEs, came in at 51.4 for September, well above the 50.2 expected.

New Zealand and Australian share markets performed well, both up 1.8% in their respective currencies. The strong performance of the New Zealand market followed what we consider one of the worst earnings seasons in recent times with multiple disappointments and downgrades to future expectations. These announcements were backed by a top down deterioration in business confidence, expectations of future trading conditions and future profits.

The theme of deteriorating business confidence was backed up by survey results with the recent releases of ANZ’s Business Outlook Survey and NZIER’s QSBO showing confidence at post global financial crisis (GFC) lows. Overall activity measures are pointing to GDP growth dipping below 1%.

It is against this backdrop that the OCR is expected to fall to 0.50% in mid-2020, with odds of a cut in November currently sitting slightly above 50%.

What to watch

Looking forward, there are three key themes we are focussing on:

- Earnings: Coming into 2019, there were concerns of a US and global earnings recession. So far this has not come to fruition with earnings holding up particularly well, especially in the US. However, downturns in manufacturing activity have historically been a negative indicator of earnings growth so we will be monitoring statements closely.

- Interest rates: Although bond yields ended the month virtually where they started, during the month we saw a sharp (c.30 bp) spike in bond yields. The resultant selloff in yield-sensitive equities, although brief, served as a reminder of the extent that low interest rates are priced into the valuations of not just bonds but also the prices of higher dividend-paying stocks.

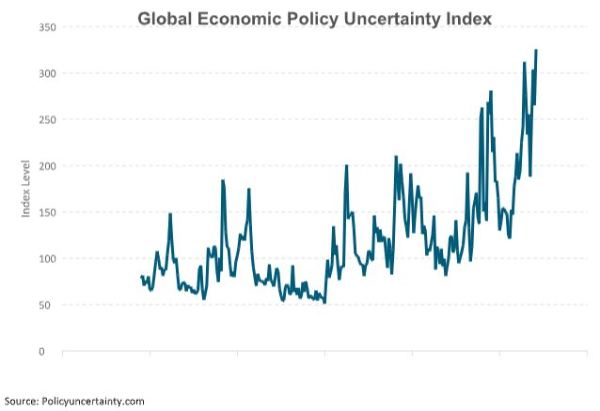

- Geopolitics: Political uncertainty has been a persistent feature over the past few years. The Global Economic Policy Uncertainty Index, which is derived using a range of measures including news articles and the dispersion in economic forecasts, is currently at an all-time high.

Market outlook and positioning

Our concerns for growth in 2020 are centred on the fall in profit expectations, negative data on global trade and falling employment intentions. ANZ's own activity expectations have fallen to -2 from a +8 reading the prior quarter, well below the long-term average of +27. Other confidence indicators are now consistent with growth in New Zealand falling below 1%.

Globally bond and equity markets continue to reflect extraordinary downward shifts in interest rate expectations. The chase for yield remains a persistent trend.

Unusually, growth stocks and some companies that may be more insulated from recession trends have not performed as well as we would expect. The Harbour equity portfolios generally remain concentrated in growth-focussed companies, with a strategy of also maintaining exposure to several larger quality defensive investments.

Within fixed interest portfolios, we are currently holding a long duration position in portfolios, expecting yields to fall across the yield curve.

However, we think it is likely that bond yields do not fall sharply from here.

The negative yields that prevail in Europe seem unlikely at present. One reason for this is that, as the OCR gets lower, technical factors in the domestic market make it difficult for banks to pass lower rates on.

This primarily happens through term deposit (TD) rates, which are a key source of funding for the banks. If banks drop TD rates too aggressively, they risk losing support as investors go elsewhere with their savings. And if TD rates can’t fall far, then banks can’t afford to drop mortgage rates much either, especially as they are being asked to raise more capital, much of which will come from retained earnings.

There is not much to be gained for the Reserve Bank of New Zealand (RBNZ) by dropping the OCR towards zero. The RBNZ is actively campaigning with the government to provide fiscal support and, as we face an election in late 2020, it is likely that we will see new projects announced.

In multi-asset portfolios, we have held our overweight position to Australasian equities.

While we are wary of valuations in this sector, we believe these equities look relatively attractive against the backdrop of low interest rates.

At the same time, we retain our underweight to global equity markets. While global equities are cheaper using headline valuation metrics, given the heightened global macroeconomic risks, we view it as sensible to take a more cautious approach within global share markets at this time.

Important disclaimer information

| « What really makes a diversified income fund run? | The importance of luck (and recognising it) » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |