Lower and lower domestic interest rates

The Harbour team examine market movements in the past month, and what they are watching going forward.

Wednesday, August 14th 2019, 6:39PM

by Harbour Asset Management

Global markets continued their rally in July with the MSCI World index (in local currency) returning 1.2%. Markets were buoyed early in the month due to a positive result from the G20 talks between Presidents Xi and Trump. The market welcomed the agreement to postpone further tariffs (the postponement didn’t last long) and keep the lines of communication open. This, coupled with a better than expected earnings season, kept sentiment relatively upbeat. The market impact of Trump’s new tariffs and China’s retaliation were captured after the end of the month.

The New Zealand and Australian share markets both outperformed their global peers, up 3.4% and 2.9% (in AUD) respectively. Strong performance from the S&P/NZX 50’s largest constituent, a2 Milk (up 22.8%), contributed the lion’s share of the overall index return. The Australian market has benefitted from the tailwinds of higher iron ore prices, a more stable political landscape and green shoots appearing in the domestic housing market.

The Fed was never far from the news in July, though ultimately disappointed the market at the end of July with its 25-basis points rate cut (markets had priced in a 20% chance of a larger cut) and its less dovish outlook. This led to some upward repricing of longer-term rate expectations, which is perhaps not unwarranted given the recent flow of economic data including payrolls, inflation and durable goods from the US has, in aggregate, surprised to the upside in recent weeks.

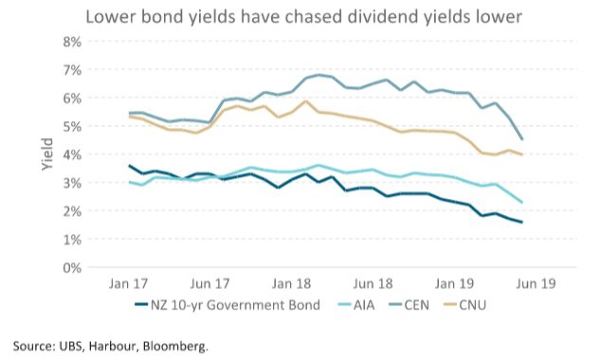

Domestically, the pricing in of lower interest rates continued in July with little good news to stand in the way of the bond market rally. July saw the release of two business confidence surveys, both of which painted the picture of a slowing domestic economy. The NZIER QSBO survey reported its lowest business confidence read since 2009, while the ANZ quarterly Business Outlook Survey pointed to some future weakness in the otherwise strong labour market. This helped pave the way for the surprise 50bp OCR cut in August.

What to watch

Economic activity continues to decelerate reflecting changing trade dynamics and the fading impact of previous economic stimulus packages. While central banks may not move to the full easing bias some have expected, they will maintain an easing bias while inflation levels remain below targets and there is a degree of under-employment in economies. Lower interest rates for longer will support the returns of bond-like equity investments, but these investments now already reflect a significant and permanent fall in interest rates. Such bond-like equity investments will need to deliver on the promise of highly dependable earnings and dividends. Investors favouring such investments will also need to watch for central banks failing to meet or exceed market expectations of easier monetary policy settings should economic activity prove to be better than expected.

Market outlook and positioning

Looking forward, geopolitical concerns, whether China-US, Brexit, Middle East or other, have the potential to continue to test investor confidence. Central banks seem willing and able (still) to respond to further reductions in activity and inflation, though central bank decisions in Europe and the US have shown that policymakers are not quite as dovish as other market participants. The impact of such events on investment markets may provide an opportunity for patient investors to invest in great businesses at what, over time, prove to be great prices.

Within fixed interest markets, with the RBNZ’s aggressive easing and bond yields at record lows, we believe that NZ fixed income assets are fully priced. While business sentiment is deteriorating, monetary conditions have eased materially, and the overall economic situation may not be as negative as the market expects. The employment market remains firm, the backdrop is supportive for housing market activity and the currency has weakened, helping exporters. We maintain a mild short duration bias relative to benchmark, but we are closely monitoring incoming data for evidence of either spill over from negative business sentiment or, conversely, signs of strength in activity. Inflation-indexed NZ government bonds continue to represent good value in the context of very low implied inflation rates and corporate bonds remain attractive.

Within our equity portfolios we are mindful that, over the long-run, earnings growth and earnings consistency drive equity returns. Recently equity market returns have been dominated by income-focused investors seeking income yield enhancement by investing in lower volatility bond-like equities as interest rates have fallen dramatically. In our view, once equity markets have repriced for lower interest rates, earnings growth is likely to reassert itself as the dominant driver of equity market returns. In the near term, delivering on earnings growth expectations is becoming more challenging for businesses that don’t benefit from positive structural trends. As a result, Harbour’s growth equity portfolios generally remain concentrated in growth-focussed companies, with a strategy of also maintaining exposure to several larger quality defensive investments.

In multi-asset portfolios, we retain a modest underweight to equities. Within equities, while we continue to marginally favour global shares on valuation metrics, the scale of the overweight is modest acknowledging that, despite favourable valuations, these shares are likely to be more sensitive to global macroeconomic shocks.

Important disclaimer information

| « Why are Australian banks investing in nuclear weapons companies? | Harvesting Black Swans » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |