Risks reduced but not removed

The Harbour team examine market movements in the past month, and what they are watching going forward.

Thursday, November 14th 2019, 8:47AM

by Harbour Asset Management

Key developments

Global equities outperformed bonds in October as trade risks abated, US earnings impressed and central bank easing supported sentiment. At the time of writing, 78% of S&P 500 companies had beaten Q3 earnings expectations and no sector had less than 58% of companies beating analyst earnings estimates.

The MSCI All Country World Equity Index (local currency) increased 1.8% while the Bloomberg Barclays Global Aggregate Bond Index (hedged into NZD) lost 0.2%.

International risks have not been removed, however, and global economic data generally deteriorated through October. Global data surprises were mostly negative, major economy manufacturing surveys remain consistent with contraction and service sector activity indicators suggest a slowing in growth.

Despite improving economic outlooks, New Zealand and Australian equities underperformed their global counterparts with the S&P/NZX 50 dropping 1.3% and the ASX 200 falling 0.4% in October. New Zealand market performance was dominated by weakness in electricity stocks after Rio Tinto announced it was reviewing operation of its Tiwai Point aluminium smelter.

Banks led the Australian market lower after ANZ reported a 3% drop in its second half profit. Weaker global manufacturing activity weighed on Australian materials companies. Healthcare, industrials and utilities were the best performing Australian sectors over the month.

Higher NZ interest rates reduced the value of local fixed income assets and the NZ composite bond index fell 0.7% in October. The NZ housing market is beginning to respond positively to record-low mortgage rates and the agricultural sector is enjoying the combination of a weaker NZD and high export prices.

Q3 non-tradable CPI inflation increased strongly and, while it was driven largely by increases in regulated prices, represented a large positive surprise to RBNZ forecasts and encouraged the market to reduce easing expectations.

In NZ, subdued business sentiment suggests ongoing lacklustre growth and inflation expectations remain historically low. The NZIER QSBO reported a net 11% of firms experienced a fall in activity in Q3 from a net 5% in Q2. Employment intentions remain poor with the ANZ survey reporting a net 8% of firms expect to cut jobs from 0% in June.

Investment intentions are also negative (-9% in September from 0% in July). Survey and market measures of inflation expectations remain well below the mid-point of the RBNZ’s 1-3% target range.

What to watch

Trade: For all the optimism about the “phase one” US-China trade deal, it hasn’t been signed. US tariffs remain in place and are scheduled to be expanded to cover all Chinese imports on December 15, increasing the average tariff from 15% to 20%. White House communication remains cautious and has highlighted several structural issues that remain unresolved between the two countries.

In the UK, the Brexit deadline has been delayed three months, but a no-deal exit remains possible and a general election will now be held on December 12, 2019, adding political uncertainty.

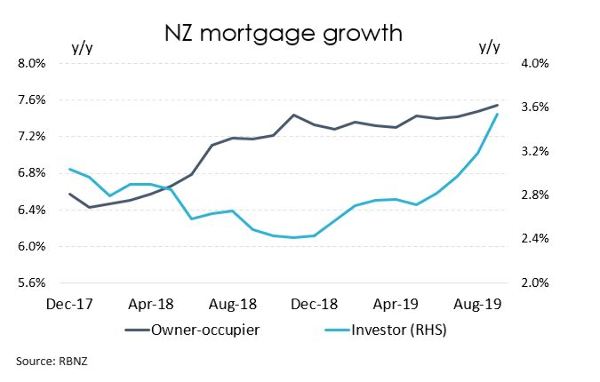

Housing: Historically low mortgage rates are beginning to translate into higher house prices and increased investment lending.

The interest rate market is poorly positioned for this to continue and increases in interest rates could be exacerbated if the large amount of upcoming mortgage renewals move to 2-year fixed rate mortgages (the lowest point on the mortgage curve) and banks hedge this risk via paying fixed rates in the interest rate swap market.

Tiwai Point: Rio Tinto announced that it is undertaking a strategic review of New Zealand Aluminium Smelter’s (NZAS) operations at Tiwai Point, to determine the operation’s ongoing competitive position and viability. Electricity generator-retailer share prices declined but credit markets took a more complacent view.

We think the risk of potential closure has increased but our base case is that Meridian and the industry will come together with a solution while also trying to achieve a positive outcome for themselves (eg contract extension).

Market outlook and positioning

We retain a degree of scepticism in the macro outlook. The global backdrop has improved but remains fragile. Domestically, large amounts of monetary stimulus have been delivered but confidence is poor and activity soft.

With this uncertainty an active approach to investment management is required. In equities, the subdued outlook for growth should favour growth stocks and the Harbour portfolios remain concentrated in growth-focussed companies, with a strategy of also maintaining exposure to several larger quality defensive investments.

Within fixed interest portfolios, we reduced duration during October in the context of an improving economic outlook but remain long relative to benchmark given soft economic activity and residual risk. Our greatest conviction remains in the appeal of NZ inflation-linked government bonds and in the poor value of New Zealand government bonds (NZGB) versus US Treasuries (UST).

Breakeven inflation rates increased 16-20bp in October but remain historically low (eg 10-year c.1%) and should continue to move higher as the domestic economy improves. Even without further capital gain, the high levels of carry make these bonds attractive to hold.

The spread between 10-year NZGB and 10-year UST yields narrowed by 19bp in October to less than 40bp but considering the respective movement in RBNZ and Fed rate cut expectations, NZGBs continue to look expensive.

In multi-asset portfolios, we have held our overweight position to Australasian equities. While we are wary of valuations in this sector, we believe these equities look relatively attractive against the backdrop of low interest rates. At the same time, we retain our underweight to global equity markets.

While global equities are cheaper using headline valuation metrics, given the heightened global macroeconomic risks, we view it as sensible to take a more cautious approach within global share markets at this time.

This does not constitute advice to any person. www.harbourasset.co.nz/disclaimer

Important disclaimer information

| « Responsible investing – why it should matter to you and your clients | Lowdown on NZ primary sector investment » |

Special Offers

Comments from our readers

No comments yet

Sign In to add your comment

|

|

Printable version |

|

Email to a friend |